💳 Fintech Goes to France

Playing Tour Guide for Fintech Business Weekly

Welcome to Startup ROI, where we explore global technology trends and how they manifest themselves in France 🇫🇷 . Whether you're an entrepreneur, investor or tech enthusiast, I'm glad to have you here!

📩 Get in touch : bonjour@startup-roi.com

New Here? Sign up for a weekly dose of French Tech:

There’s a certain kinship among expats making their way in a foreign country. And there was certainly no exception with today's co-author (and fellow American), Jason Mikula, who writes Fintech Business Weekly. His newsletter is exactly as advertised: in-depth coverage of the ever-changing fintech landscape. I admire his precision, attention to detail and depth of knowledge on the subject. If you haven't already, do yourself a favor and subscribe to stay on top of one of the fastest growing categories in technology today!

France: A Quick Geography Lesson…

Given the country’s outsized role in world history, you’d be forgiven for thinking it has a larger population than it actually does. As of 2020, France boasts a population of about 67 million, making it the second most populous country in the EU, behind Germany.

France, an economic powerhouse in the EU, also comes in second when measured by GDP, again behind Germany, at USD $2.63 trillion. Despite Americans’ perception of Europe in general and France in particular as having a generous social safety net, its poverty rate is 13.6% – ahead of the US’ 11.4% (note: definitions of ‘poverty’ vary and both metrics pre-date the coronavirus pandemic).

Banking in France – A Concentrated Affair

France boasts 337 banks – which, if you’re used to the American banking market, probably sounds low. The US, with ~5x the population, has nearly 15x the number of licensed banks (and that doesn’t even count an additional ~5,400 credit unions).

It should be unsurprising then that banking concentration is substantially higher in France than the US; the largest three banks – BNP Paribas, Crédit Agricole, and Société Générale – hold a whopping 57% of assets in the banking sector. While the US is also dominated by large banks, the biggest three hold a comparatively small 35% of total assets.

Like most of the Western world, the number of bank branches has been steadily declining as adoption of digital banking channels increases. The number of bank branches per 100,000 adults has declined from 45.9 in 2006 to 33.2 in 2020, compared to 29.7 per 100,000 adults in the US in 2020.

Consumer banking penetration is extremely high, with 94% of adults over 15 having access to a bank account – though this has actually dropped 2% points since 2014, according to World Bank data.

Credit card usage in France is markedly lower than the US. While 66% of American adults own at least one credit card, the proportion in France is just 41%.

French Financial Life: La Vie En Rose

Perhaps ironically, culture is one the toughest forms of capital to quantify. Culture influences everything from fashion to art to food. It both informs and signals our identity. Broadly speaking it impacts economic behavior: consumer spending, risk-aversion, socio-economic stratification, and savings goals to name a few. Which is why it's important to consider a country's culture when evaluating their financial system. We already stated that France is an economic powerhouse — and certainly boasts world renown for the aforementioned fashion, art and food categories — but let's explore some other cultural elements that contribute to a unique fintech ecosystem.

The French are no strangers to bureaucracy, but the tradeoff provides some fairly cushy state benefits that most Americans would salivate over. The French government (trigger warning: they're socialists) plays a comparably outsized role in the lives of its citizens and arguably for the better.

Free healthcare ensures quality access and a healthier populace (reducing risk of crippling health-related debt or bankruptcy) — Kyle wrote about the French healthcare system in detail for the policy wonks out there

A public pension scheme provides labor force participants with a forced savings mechanism and guaranteed income post-retirement

Stringent labor laws and unemployment benefits offer job security and a cushion for the less fortunate (the flip side? not so great for doing business)

An emphasis on higher education through public schools at reasonable prices (average tuition by country listed below)

The social safety net is undoubtedly more robust (and less stigmatized) than in the US, which might lead you to think French consumers would be somewhat spendy. But as it turns out, the French are thriftier than you might expect. According to a report from BNP Paribas, they outpace the average savings rate in the eurozone and rank #1 among the major economies in the region:

“France (14% in 2018), behind Germany (17.9%) and the Netherlands (15.1%), is the major eurozone country with the highest household savings rate (average of 12% across the eurozone).”

For context, that's on par with the personal savings rate in the US at the end of 2020 (13.7% according to the Federal Reserve research), though somewhat misleading due to the COVID-19 pandemic savings boom — a typical pre-pandemic rate in the US was ~7%.

Which brings us to our final cultural flashpoint that distinguishes the US and France: living within your means.

One might attribute this to differences inherent to a capitalist versus socialist society. But I would argue that's not quite right. You see, the French enjoy the finer things in life, in fact, they savor them. French cuisine, domestic wine, an evening with close friends and family. When it comes to experiences, especially with loved ones, paying a premium is tolerated, even welcome. But it's about the company and quality of the experience, not a materialistic display of wealth.

The “American” dreams of a new Rolex, a bigger house than his neighbor, or an ostentatious vacation home; the "Frenchman” dreams of a vintage Rhône Valley bottle of red, a pied-à-terre in Paris housing philosophy books, and a yearly trip to a modest, clandestine beach destination. It's subtle, but different.

The catalyst that enables this spending discrepancy is somewhat obvious to those living abroad: consumer credit. You can't go an hour in the US without being bombarded with adverts for a personal loan, buy now pay later product, or new credit card offering a huge signup bonus, giving you the opportunity to acquire the next shiny object on your list. Here's the thing: credit cards don't really exist in France. You have what's called a Carte Bancaire (CB) that works like a debit card, but getting a line of credit is reserved for rare occasions:

Buying an appliance at Darty (yes, the French version of Best Buy sounds like a day-drinking event at a sorority) that offers revolving credit

A home loan or mortgage (emprunt immobilier), the preferred wealth-building method of the French, as we'll explore later

Traditionally, for those day-to-day purchases, it was more challenging to find credit, requiring a trip to your local bank and a mountain of paperwork. Today, thanks to several emerging players in fintech offering micro-loans or BNPL, that is beginning to change, and even significant purchases can be financed through a digital platform at modest interest rates

So despite a vast social safety net and a dearth of consumer credit (at least as we Americans perceive it), the French save more and buy less. Your average microeconomics professor might be stumped, but even a novice social anthropologist could trace it back. There's a saying in France, popularized by the Edith Piaf song: La Vie en Rose (life through rose colored glasses). The idea is to see the beauty in life, the simple things, even when times are tough an apt expression that one might surmise is baked into the culture itself.

Yes, More Regulation – But That’s Not Always a Bad Thing!

At this point, it’s a bit of a worn cliche to bemoan the bureaucracy in Brussels, the location of the EU’s executive body, the European Commission. Given the organs of EU governance are charged with formulating and implementing policy across 27 discrete countries, that the wheels of its bureaucracy turn slowly shouldn’t be too much of a surprise.

In general, approaches to regulation are formulated at the EU-level by European supervisory agencies (ESAs), which include the EBA for banking activities, the ESMA for financial markets, and EIOPA for insurance markets. These EU-level formulations are guided by global recommendations from bodies like the Basel Committee (safety and soundness) and the Financial Action Task Force (financial crime/money laundering).

ESAs develop regulatory technical standards, implementing technical standards, and Q&As that guide implementation by national-level governments and regulators; the goal is to achieve consistency in implementation across EU countries.

In France, the two key regulators are the Autorité des marchés (AMF, the financial markets authority, somewhat comparable to a combination of the SEC and CFTC) and the Autorité de contrôle prudentiel et de régulation (ACPR, the banking and insurance authority, roughly approximate to the OCC, FDIC, parts of the Fed, and state insurance regulators rolled up into one).

Going into the full scope of EU directives and French implementing laws and regulations is beyond the scope of this humble newsletter, but it’s worth reviewing the elements most relevant to the fintech ecosystem.

France’s Fintech- and Crypto-Friendly Licensing

‘Traditional’ Bank License

A traditional banking license (“credit institution”) is required to hold deposits, engage in banking payments, or engage in credit transactions, though specialized consumer finance firms associated with retailers/auto and, more recently, peer-to-peer lending also exist under different licenses.

Crowdfunding & Crowdlending

Dating to 2014, France created a framework for crowdfunding (equity or debt investments) and crowdlending (peer-to-peer lending). France’s crowdfunding framework is roughly analogous to the US SEC’s Regulation Crowdfunding. France’s regulation of crowdlending provides a significantly streamlined licensing and regulatory approach vs. what needs to be navigated by the few remaining American peer-to-peer lenders like Prosper.

Payment Institution / e-money Institution

French regulation permits licensing of payment institutions and e-money institutions, which are the frameworks under which French “neobanks” operate – though note that in 2021, the ACPR prohibited use of the term ‘neobank,’ arguing that because firms in this category are not licensed credit institutions (banks), they cannot use this term to describe themselves (not unlike Chime’s run-in with California’s DFPI).

Capabilities of payment institutions and e-money institutions include:

Services enabling cash to be deposited into or withdrawn from a payment account and the transactions required to manage such an account;

Execution of payment transactions associated with a payment account (card payments, credit transfers and direct debits);

Transmission of funds;

Payment initiation and account information services;

Issuance of means of payment and/or acquisition of payment orders.

A simplified licensing procedure is available for payment institutions processing less than €3 million per month and e-money institutions processing less than €5 million per month.

The result is an easier, faster, cheaper licensing model for nascent fintechs that avoids the complexity and regulatory uncertainty of the bank partnership model leveraged by US neobanks.

Digital Asset Service Providers (eg, crypto)

The PACTE Act of 2019, amended in 2020, creates a new category of entities known as Digital Asset Service Providers (DASPs). Services entities in this category may offer include asset custody, exchange cryptocurrencies for fiat and vice versa, digital asset trading, and a variety of other related services. Some aspects of the licensing framework are optional, though asset custody and exchanging to/from fiat require registration with the AMF.

This arguably compares favorably to the US, where there remains no crypto-specific legislation/regulation whatsoever and, instead, regulators apply existing frameworks, some of which date to the 1930s, to the rapidly evolving digital asset space.

Robinwho? Savings and Retail Investing in France

In the US most folks are comfortable with terms like 401k, Roth IRA and index funds, but the recent upswing in day trading brought on by neo-brokerage apps like Robinhood has redefined the retail investing category.

Anecdotally, I've witnessed more acquaintances in the US enter their hat in the ring, tempted by volatile markets and a penchant for the dopamine hits associated with winning big. Americans don't have a monopoly on gambling by any means, but if I were a betting man, the get-rich-quick mentality surrounding today's financial markets just isn't as appetizing or accessible in France. In fact, the two most popular savings channels in France are quite conservative by comparison: the Livret A and the Assurance Vie.

*Note: this is an oversimplification of savings/investment methods, but I'm sharing the mechanisms most commonly used.

Livret A

The Pros: A short term savings vehicle with low interest rates (.5%), no fees, and 100% guaranteed (i.e. risk-free) and exempt from social security taxes

The Cons: Maximum total deposit of €22,950 for individuals, a fairly pathetic return (doesn't even outpace inflation), it's primarily a holding pen for cash looking for better than zero return but seeking a higher yield investment

Key Stat: 9/10 French citizens have a Livret A

Fun Fact: This financial innovation was created in 1818 and was accessible to everyone with a 2000 franc cap and a 5% interest rate

Assurance Vie

The Pros: Higher interest rate (closer to 2% depending on the offer/year), better service from the bank, the capital is deployed (instead of sitting in a checking account) and you have say in where to deploy it, you can choose a beneficiary in the event of your death, tax exempt for the duration of the contract, capital is guaranteed 100%

The Cons: it's an 8 year commitment (can't touch it!) and may incur service fees depending on the plan you choose

Key State: Only 37% of French citizens have invested in an Assurance Vie

Fun Fact: In the late 1700s life insurance policies were considered "reprobate and against good morals" by the Ordonnance de Colbert (it wasn't until 1818 they were legalized)

That said, the immense progress in digital banking and neo-broker market penetration is shifting the landscape. Investing directly in the Bourse (stock market) is more accessible than ever through online brokers and high throughput trading apps (Robinhood doppëlgangers) have onboarded a new generation of millennial and Gen Z investors right from their mobile device.

Interchange, Open Banking & Other Key Regulatory Differences

Interchange

The EU, including France, lack a regulatory quirk that has powered a good chunk of US consumer fintech innovation: debit interchange. While interchange for debit cards issued by small banks (<$10 billion) in the US remains uncapped, in the EU, transactions are typically capped at 0.2% – a far cry from the ~1.5% common in the US.

The stark difference in interchange revenue, while undeniably a benefit to French merchants (and, by extension, consumers), provides French fintechs with fewer paths to monetization.

PSD2 / Open banking

“Open banking” in the US has evolved quite differently than in the EU. The EU has taken a regulatory-led approach, in the form of PSD2 (payment services directive), whose original intent was to promote competition and innovation by requiring banks to provide secure APIs to share customer data and enable third parties to initiate payments. In the US, so far, open banking has been market-led, in the form of private banking connectivity providers like Plaid and MX, though the CFPB is beginning to undertake rulemaking as called for in Dodd-Frank.

Passporting

One of the most appealing benefits of operating in the EU is the ability to “passport” a license granted by one country’s regulator to operate in other countries. This can be done by opening a physical branch in another country (freedom of establishment) or without a physical presence (freedom to provide services.)

European neobanks like N26 and bunq, which are fully licensed banks in their respective home countries, leverage passporting to operate in multiple European countries. More recently, Revolut was awarded its Lithuanian banking license, and is in the process of transitioning European customers from its e-money institution entity to its full banking entity.

CBDC: A Digital Euro

Like seemingly every central bank these days, the European Central Bank (ECB) is studying the pros and cons of introducing a Euro central bank digital currency (CBDC). The ECB kicked off a 24-month project to investigate the issue, though current ECB President Christine Lagarde has said the launch of such a project would take at least five years.

Other Policy & Regulatory Issues: Antitrust, GDPR

In addition to finance-specific considerations, there are a number of other regulatory (and political) areas shaping the business environment in the EU and France. The EU has long had a more robust posture on antitrust than the US has, particularly when it comes to foreign entities doing business in the EU. This can be seen in actions against “big tech” – Google, Facebook, and Microsoft. Establishment financial services players, like Visa and Mastercard, have drawn their share of scrutiny as well.

Companies in the fintech sector, though much smaller than these examples, have begun to draw scrutiny as well – particularly as it relates to how markets and market power are defined.

The EU, and thus France, also have a substantially more robust privacy and data protection framework than the US, in the form of the General Data Protection Regulation (GDPR), which went into effect in 2018. A deep-dive on GDPR is beyond the scope of this post, as the regulation is expansive, complicated, and can result in fines running into the tens of millions of euros for non-compliance (Google has been fined at least €100 million for violation of French rules on tracking cookies, for example) . The closest US analogue is the California Consumer Privacy Act (CCPA).

Examples of How Fintech is Helping French Consumers Navigate a Changing Financial Landscape

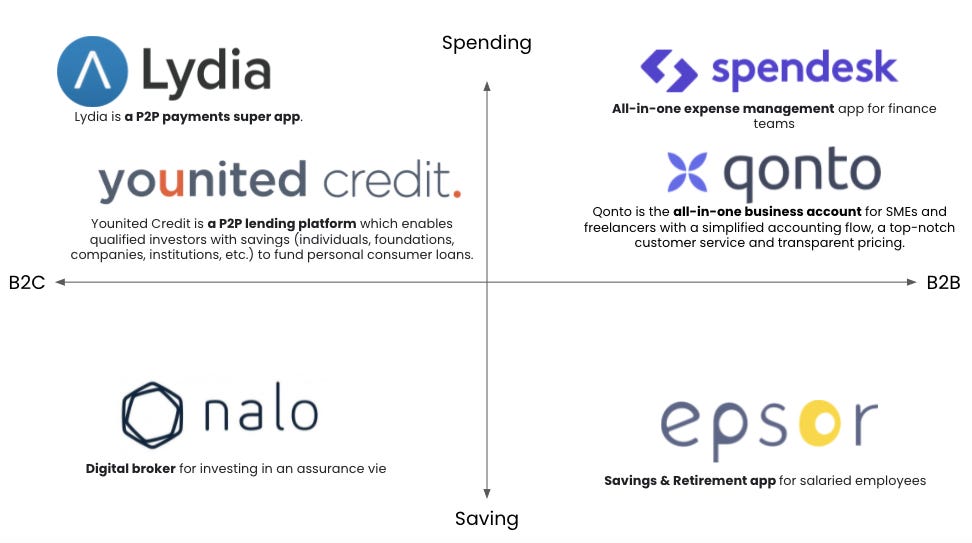

Younited Credit: the Prosper of France

Younited Credit is a peer-to-peer lending platform connecting qualified investors with individuals seeking personal consumer loans. The lack of consumer credit in France leaves a big gap between day-to-day purchases and the higher end business loan or mortgage. Younited Credit fills that gap for midsize personal loans for anything ranging from a car purchase or home renovations. They offer lines of credit as low as €1K and max out at €50K with 8 options for the payback period (6 - 74 months). Their USP is speed and transparency. You might compare them to a Prosper or Lending Club in the US (before LC shuts its retail investor platform, anyway).

Spendesk: the Expensify of France

Spendesk is the all-in-one expense management app for finance teams. If you've ever worked at an SME, you understand the pain associated with provisioning corporate cards, tracking budget and handling expense reports. Spendesk furnishes virtual cards, expense management tooling and workflows for approvals and reporting. A close cousin in the US would be Expensify.

Qonto: The Bank Novo of France

Qonto is the all-in-one business account for SMEs and freelancers. The French fintech darling recently raised a €486M Series D, valuing them at €4.4B with the goal of reaching 1M SME customers by 2025. In a growing European startup ecosystem, demand for simple and intuitive products to power your business is skyrocketing. Qonto offers services ranging from creating your business, automated bookkeeping, expense management and more. Bank Novo is a close analog in the US, with Brex and Ramp falling within a similar category.

Lydia: The Venmo of France

Lydia is the leading P2P mobile payments app of France (and soon-to-be Europe). In the US you might ask someone to Venmo you; in France Lydia has become a verb as well. They've recently rolled out premium plans with current accounts and additional services (Lydia Blue & Black) and have ambitions to become the financial super app of Europe.

Unlike Venmo or Cash App, Lydia remains independent (the US counterparts are divisions of PayPal and Square, now Block, respectively). In December of 2021, shortly after announcing stock and crypto trading functionality, Lydia raised a $100M Series C, cementing unicorn status.

Nalo: the M1 Finance of France

Nalo is a digital broker for the Assurance Vie investment vehicle we touched on earlier. With a minimum €1K investment, you can easily navigate various curated funds to invest your nest egg. Think of it like a verticalized Fidelity with hints of digital-native robo-advisors like M1 Finance, Betterment or Wealthfront.

Epsor: The Blooom of France

Epsor is a savings and retirement application for salaried employees. In the US, offering a 401K plan can be costly and complex for a small business. This problem isn't unique to American entrepreneurs. Epsor combines algorithmic and human-centric advisory services to structure a savings and retirement plan (as a benefit or perk) for their customers' employees. The funds they offer lean towards the eco-responsible and they supply additional services and consulting to ensure individual needs are met. Blooom, a US company, offers a similar service with 401K and IRA management for small businesses.

The Closing Bell (Conclusion)

I hope you enjoyed this foray into the world of Fintech in France. This piece wouldn't have been possible without the subject matter expertise of Jason. For more on all things fintech, subscribe to his weekly newsletter.

If you’re like us, you will enjoy this economics-themed-meme. It's a pretty good litmus test for subscribing to our newsletters!

| A guest post by

|