🩺 Insuring the Future

Alan and the digital health transformation France didn't know it needed

👋🏼 Welcome, readers, to the very first installment of Startup ROI. You are a member of a new community set on discovering how global tech trends manifest themselves in France. I can’t tell you how grateful I am that you’re supporting this project, and I’m serious when I say I want your feedback. If you like today’s essay, please share it with a friend you think may find it as relevant/interesting as you did. If you’re new here, subscribe to hear from me weekly!

Before we start, a quick apéritif ! Here's a synopsis of what you’re about to read:

✏️ Today’s essay covers: an up and coming healthcare technology company based in Paris called Alan. It was started by Jean-Charles Samuelian-Werve (heretofore referred to as JCSW) and is the first digital health insurer to receive a license by the requisite French governing body in quite some time #spoileralert

🚀 What makes Alan disruptive? Well, a lot. More specifically, it’s their ability to navigate complex regulations, their digital-native / app-first approach to health insurance, and their expansion strategy, which I argue starts with one of the hardest parts (approvals/regulation) in an effort to expand into slightly easier (thought still very difficult) areas of the healthcare services ecosystem

💰 Why it matters: Alan recently closed a €184 Million fundraising round with a valuation of €1.4 Billion. They are on their way to becoming a tech juggernaut not only in 🇫🇷 France but 🇪🇸 Spain and 🇧🇪 Belgium as well. Their unconventional tactics, unique culture, and rapid iteration may be the model for future health-tech companies launching around the world

Introduction: A "Healthy" Business

Like many a modern executive, Jean-Charles Samuelian-Werve (JCSW), CEO & Co-Founder of Alan, released a book outlining his philosophy and learnings derived from starting a company. "Healthy Business: A Corporate Culture of Wellbeing and Excellence" was published in 2020 and espouses personal theories, first-hand experiences, and a curation of quotations, references & frameworks from the tech giants who inspired JCSW. It serves as a manifesto for startup culture, the future of work and perhaps most importantly a roadmap to better outcomes for society both inside and out of tech's elite circle. Its ethos reminded me of a famous proclamation from Marc Benioff, Chairman and CEO of Salesforce.

"The business of business is not business,” according to Benioff. “The business of business is improving the state of the world."

Like Benioff, JCSW has a penchant for idealism with a hint of showmanship. Arguably, the two are also laser-focused on hyper-growth and unprecedented success which, put in practice, tends to be at odds with their utopian vision of work/life balance. But I digress...

In the introduction of his debut book, JCSW makes reference to a scene from "Alice in Wonderland: Through the Looking Glass" in which Alice and The Red Queen appear to be running in place despite all efforts to the contrary. The lesson? The world doesn't stand still for anyone. To be a part of it, you need to keep moving, you need speed. You have to run just to stay in place. The metaphor suitably conveys the challenges of a new entrant into a dizzyingly complex and oftentimes archaic industry. In this essay, I'll uncover Alan's approach to revolutionizing healthcare and how they plan to build stamina on the treadmill of innovation.

Domestically, Alan has positioned itself orthogonally by tackling one of the hardest problems first (navigating bureaucracy and disrupting an incumbent oligopoly) with a plan to layer on services across the value chain. Abroad, they're coming from a different angle. The result generates two flywheels spinning in opposite directions that amplify Alan's brand equity, product stickiness, and differentiation in the market. While none of these lines of business are inherently unique, Alan has created a platform in which the whole may be more than just the sum of its parts, but a multiple of it.

The State of Healthcare

The global health crisis in which we find ourselves today has prompted many of us to take a deep look in the mirror and reconsider our priorities. I, for one, am committing to spending more time with family and friends (and have entered my hat in the ring as a niche, tech-newsletter author/modern media company founder… *laughs nervously*). So where better to kick things off than with an essay on health-tech, more specifically, health-tech in France, it’s implications for the existing system and why it’s fundamentally different from what we’ve seen emerge in the broader startup ecosystem (both here and overseas) over the past several years. As you can imagine, Healthcare policy is a complex (and tbh, dense) subject, but there are some elements that are critical for understanding the thrust of this article.

Let’s start with something relatable: pandemic response strategies. In the early stages (circa March 2020), it appeared as if France was taking appropriate measures to “flatten the curve” -- they implemented serious restriction of movement and galvanized a show of support for frontline workers. Meanwhile, in the U.S., mask-wearing was politicized and the president was actively campaigning against the measures recommended by the CDC. From abroad, the US looked like a public health dumpster fire; I can’t say that testing and contact tracing efforts were flawless in France, but at the very least people wore their masks without protesting about their civil liberties (and believe me, the French love both protesting and their civil liberties). In a breath-taking turn of events, however, under the Biden administration, the US has regained its footing and launched a vaccination campaign that has outpaced everyone’s expectations.

Above: Vaccination Projections in the US, Source: NY Times

We can all agree that we’re (hopefully) at the end of this global catastrophe, but I know what you’re thinking: pandemic excluded, what does the Healthcare System look like in France? What are the key differences between the American & French system? And finally, who cares? I’m glad you asked:

The French system prides itself on being universal. In fact, the French view healthcare (as do, arguably, most progressives in the US) as a fundamental human right. I’ve even overheard frustrated peers in New York say things like “ugh, our system is bullshit, I should just move to France because everything is free.” And, for the most part, that’s true. But there is some fine print worth highlighting. The modern French system, known as “Securité Sociale'' was established after WWII in 1945. Since then, there have been amendments, improvements, unions/organizers and bureaucracy put in place… but generally speaking, it’s the same foundation. Essentially, everyone has access to it as long as you're registered in the country in some capacity (through work, your university, or even via unemployment). What Securité Sociale offers is access to “basic and/or common needs” (think check-ups, injuries, cancer treatment). Sounds ideal. But there’s a catch: what qualifies for “basic needs” is determined by a committee and is subject to change. This independent public body, called the Haute Autorité Santé, carries out a range of missions and acts autonomously although it liaises closely with the French government.

While they hold themselves to rigorous scientific standards, there are undoubtedly some human biases at play here. For example, you want to start taking Birth Control? Nope, not covered. Certain Alzheimers treatments? Not so sure about the science there… From personal experience, I had to switch antidepressants from Wellbutrin (a stimulant) to Prozac (an SSRI) due to the prevailing theory in the French medical community that prescribing stimulants is a faux-pas. One was free, and one was costly. I paid out of pocket, and frankly, it was hard to find a doctor who would prescribe it or a pharmacy that had it in stock. That said, a ride in an ambulance or a stay at the public hospital won’t cost you a centime.

But Kyle, I thought this essay covered a digital health insurance company… Why the heck do they need insurance if virtually everything is free? 🤷🏻♂️

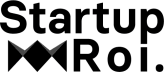

I was asking myself the same question about 3 years ago when I arrived in Paris. I still remember going to the pharmacy for the first time and handing over my prescription. When the pharmacist gave me the meds and swiped my carte vitale (state issued insurance card), they just told me to leave. No co-pay or anything. I felt like I was robbing the place. So when my HR Manager asked if I wanted to sign-up for the company mutuelle (read: supplementary insurance), I was bewildered. “You have problem with ze teeth?” he asked. Well, no, not at the moment, I thought. But, counter-intuitively, there were more things that fell outside the scope of basic universal coverage: dental, vision, certain providers depending on their “sector.” To avoid going too deep on this, let’s just say that supplementary insurance is recommended (especially if your company helps pay for it). We’ll see why later on, but in the meantime, here’s a quick chart to break down the complexity.

Above: Coverage depends on the “sector” of care (1) covered universally (2) covered in full or in part by your supplementary insurance (3) not covered. Free (Sector 1) isn't always better — occasional long wait times, specialists may be located far away; Out of pocket (Sector 3) may help you skip the line but will cost you; middle ground (Sector 2) gives you optionality, pay a slight premium for convenience/quality and if you have a “mutuelle” most if not all will be covered. Allianz, Malakoff, & Generali are three of the dominant players in the insurance space today.

As you may have guessed, the goal here isn’t to dissect the French Healthcare system. There are some positives (mostly free) and some negatives (arbitrarily subject to additional insurance, bureaucracy, & paperwork, like lots of paper that you can NEVER throw away under any circumstance). If you want a quick dose of humility (I’m talking to my fellow Americans), watch this NY Times video showing foreigners react to the atrocities committed by our own system.

OK, so we’re even in terms of country-specific criticism. No harm, no foul. Let’s move on to the good stuff!

The Status Quo - Rien N'a Changé

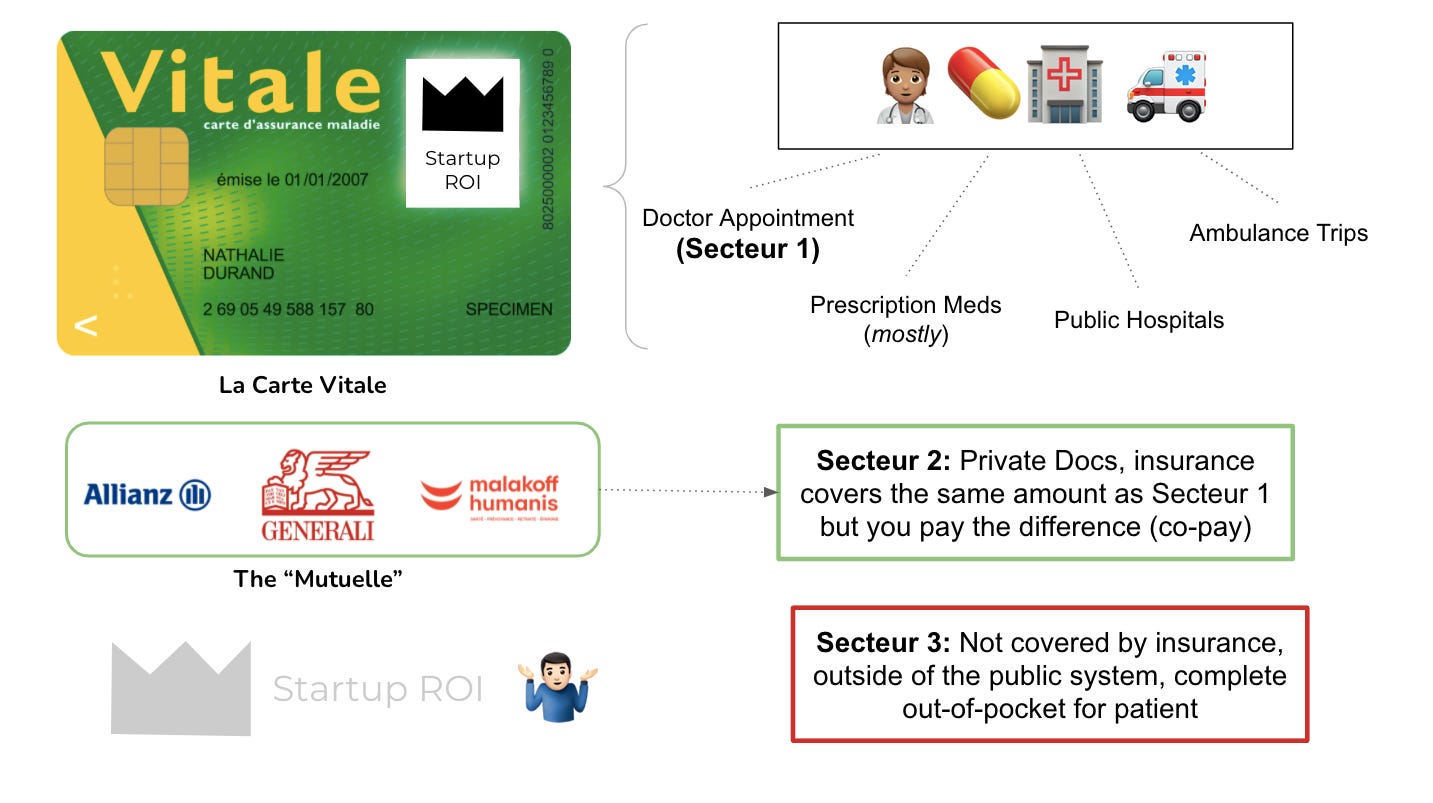

The last time a company received a health insurance license in France took place in 1986. NINETEEN EIGHTY SIX! That’s about three decades of dominance among the oligopoly highlighted in the graphic above. It’s also worth noting that 96% of the French population has some sort of private, supplemental health insurance. It’s a €50B market that has seen little to no innovation. And in terms of UX (you guessed it) it's absolute garbage. Let’s have a look at the typical “user experience” when claiming a reimbursement:

Above: The “Old Way”

I doubt there was any collusion among the big three insurance companies to keep their moat wide & deep. But they didn't seem to have to work hard to keep it that way. It was virtually impossible (or I should say, unthinkable) for newcomers to enter the market. So who in their right mind would attempt to disrupt a highly bureaucratic, policy-heavy, private/public institution that’s been around for nearly a century?

Enter: Alan, the first digital healthcare startup to challenge the French regime of old-school insurance companies.

The “Radical” Founder

JCSW may speak in hyperbole, but for some reason you get the sense that he’s the one who can will this company into existence. JCSW is unapologetically international (and dare I say, American? In the sense that he appears to be a Silicon Valley acolyte…). He’s got a Substack, he promotes radical transparency at the company, he’s implemented a “no meetings” policy. Not to mention, he has virtually no experience in healthcare. In line with this entrepreneurial ethos, you can find blog posts touting new frameworks for decision-making or pictures from a team retreat in Tenerife, complete with post-its clouding your view through a window to the beachy sunset. Omni-present on Twitter and Clubhouse -- he seems to possess unlimited energy, especially when he’s passionate about a subject.

Not unlike many founders, his background contains some mythology. But here are the key facts:

He studied at École des Ponts -- a highly regarded STEM focused university outside of Paris

He launched his first business venture, Expliseat, while still an undergrad. The idea? Redesign an airplane seat out of carbon fiber & titanium to reduce the weight from 13kg to 4kg, thus saving an extraordinary amount of carbon emissions per flight.

As the story goes, six years into the venture his grandfather was diagnosed with Cancer. JCSW oversaw his care and realized, through all the paperwork, that there had to be a better way to supply health insurance in France.

He put together a business plan and gathered his closest startup companions (and healthcare/insurance experts) to put things into motion

They obtained the requisite healthcare insurers license for Alan (l’ACPR: Autorité de contrôle prudentiel et de résolution)

Alan raised a seed round of €12 million in 2016

Since then, they’ve been in hyper-growth mode. I remember the French startup where I worked switched from Malakoff (legacy player) to Alan in 2018, and at first I was confused… why is this better? What I’ve found is that the user experience is just the start.

The New Kid on the Block

You’ve got the full picture. Old industry, new player, incumbents are a bit shook but probably thinking can this kid really get a cut of our business? After all, the French public had been submitting paper files for decades without complaint (it should be noted that the French are fairly accustomed to bad UX and stacks of paperwork). The ingenious insight here came from real-life experience. JCSW was young, tech-savvy and born into internet culture -- if he's having a bad experience, his peers must be too. Alan just needed to get young, independents on board, then maybe they could convince startups and eventually enterprises to change tack as well. Not only could they prove the value, but their employees would demand it. They pulled off a fairly remarkable rise to prominence (+160K members) in a very short period of time. Here’s how:

Above: Alan's range of product offerings (insurance & beyond)

Digital First & Emoji Heavy

This may seem fairly obvious (because it is), but applying digital transformation to antiquated industries is generally a win. That doesn’t mean it’s not hard. With a mobile app, a clean interface, and plenty of emojis for our millennial and gen-z friends to feel at home, Alan has cultivated a fan-base. Not to mention, it’s marketing team has followed suit with a friendly/casual tone -- significantly more approachable than the insurance giants that preceded it. They’ve got a cute mascot too. Which I’ve confirmed is a marmot, however, I’ve personally confused it for a sloth, koala and (because of the emoji on JCSW’s twitter profile) a panda bear.

Paperwork to Paperless

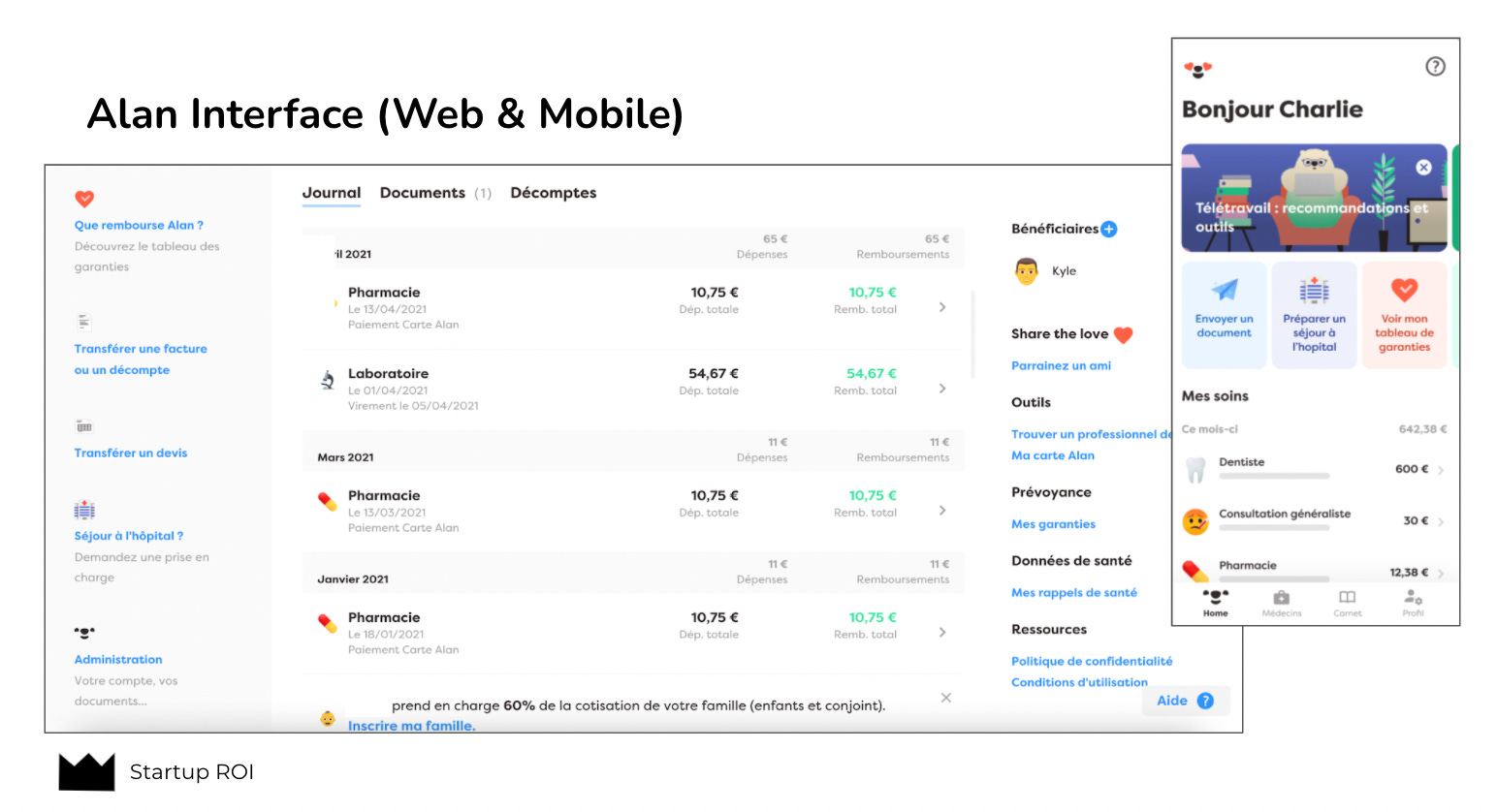

I cannot stress this value prop enough. In some cases, when all goes to plan, you can swipe your carte vitale and you’re good to go. If, however, you go to the wrong doctor, or a doctor who doesn’t have the swipey-machine-card-reader-thing, or there is some unexpected prescription that isn’t quite covered etc., the paperwork gets ugly, quickly. I’m probably biased because filling out opaque health forms in a 2nd language is absolutely soul-crushing, but that’s not the end of it. You’ve got to send it into the right processing center depending on where you live (try googling it…). You’ve got to physically go to the post-office (the French hate the post-office just about equally to how much they love talking about how much they hate the post office). Then, hopefully if everything gets processed you can log into the public health portal (Ameli) and check to see if/how much you got reimbursed. Look, I don’t need to sell you on this. The other day, I took a picture of my contact lens receipt and uploaded it to the Alan app and was reimbursed in under 48 hours. Before Alan, there were times I ate the out of pocket expense just to avoid the headache of filing a reimbursement claim. The experience is literally night and day.

Above: The “New Way”

Brand Equity & In Your Face Marketing

There was a point in time where you couldn’t take a trip out of the house without running into an ad for Alan. For you New Yorkers, you may remember the subway takeover of brands like HIMS/HERS or Casper mattress. Alan took a page out of their marketing playbook. The copy was fun, clever, and cute, which is a change of pace from what you typically see in the Paris Metro.

Above: (left) Bottom-up approach to growth, starting with independents and moving up to the enterprise; (right) Alan ad campaign in the Paris Metro

Land and Expand

As I mentioned earlier, the bottom-up approach was a critical lever for growth and adoption. Target individuals or part-time/gig workers first and let them spread the message for you. Easy to register, easy to use. Boom, you have a solid base. Paired with a massive paid campaign, it wasn’t long until startup workers were like “ahem, I’ll have what they’re having…” Onwards and upwards to the big enterprises 📈

Above: €310M raised over 5 years (Seed to Series D) with a current valuation over €1B 🦄

People LOVE this brand. It’s a total 180° from the previous experience. I shit you not, they have an eCommerce site with branded gear that anyone can buy. Can you imagine if, like, Blue Cross, Blue Shield sold merch!?

Above: Merch store on the Alan site (you, too, can own a plush marmot toy, branded socks or a t-shirt!)

The Polar Vortex Flywheel

Anyone who’s been in a business or entrepreneurship class has likely seen a pitch where someone states: “the TAM is about €50B so even if we just get 1% of the market, we’ll capture €500 million in revenue.” To which the professor likely shakes their head and quietly fantasizes about the double martini they’ll be downing after class. The point being, that with all that funding, the operational costs, the follow-on competition and the pushback from legacy players will necessitate Alan to expand beyond France. The difficulty, however, with their approach in France is that it’s really hard. You can’t just rinse-and-repeat the disruption of a legacy public/private insurance system, especially when regulations differ across borders and internationalizing operations pose unique obstacles (language barrier, culture, more existing players/competitors, compliance). So what to do?

In the Q1 Shareholder announcement (that Alan publishes on their blog #radicaltransparency), they’ve hinted at the roadmap. And interestingly, they are taking the exact opposite approach in foreign countries. In France, they disrupted the system, acquired users and brand equity, expanded into the enterprise and just now are planning to offer additional lines of business in the form of services. In Spain & Belgium, their next two targets, they are building out telehealth units and appointment booking systems. In this way, they can drive adoption but continue to avoid regulatory hurdles for the near-term. Eventually, they can backward integrate into the insurance industry. In a way, they’ve got two flywheels spinning in opposite directions -- but instead of counteracting one another, they actually intensify the system. I call it the Polar Vortex of Flywheels:

I'm confident that Alan has the wind at their back. Having crept onto the scene in France, and despite little brand recognition outside the country, they have a clear opportunity for growth. But their greatest weapon may also be a weakness when they aren't on their home turf.

The Trojan Hearse

Alan is sneaking it’s way into the European market; and my instinct tells me they are going to slowly but surely escort out the legacy players (or at the very least drive major change). While they have a lot of the puzzle pieces in place, they remain young, relatively regional and have a long road ahead with plenty of obstacles. In the glow of their recent unicorn fundraising round, it can be difficult to take a step back and acknowledge the bear case. For posterity, let's evaluate some of the risks involved in attempting to become the healthcare super-app of the future:

Scale: In France, about €1.5B was invested into health tech companies in 2020. For comparison, the US saw a staggering $15.3 billion in venture money put towards the same sector according to a report from Silicon Valley Bank. To be a global player, they are going to have to compete on the global stage. While Alan may be the prodigy of French Tech, they aren't the only show in town.

Regulation: Alan made history in France as the first entrant into the insurance market in decades. Can they repeat that abroad? Can they sustain themselves in foreign markets without their core insurance product? As Ben Horowitz (who happens to be admired by JCSW) so eloquently shared in his book “The Hard Thing about Doing Hard Things” : If you are going to eat shit, don’t nibble. I get the impression there will be quite a bit of shit-nibbling across these new markets. Do-able, but unpleasant.

Sub-verticals: "Health-tech" serves as an umbrella term for a multi-trillion dollar industry worldwide. To attempt an industry map would be a futile effort, but fortunately, there are plenty of industry reports dedicated to categorizing the various areas of focus. I'd like to touch on three in particular that give some context around the global health-tech landscape but also align quite closely with Alan's ambitions for it's expanding product suite. I'll do so by evaluating market leaders in each sub-vertical.

Insurance Disruptors

Digital Front Door & Patient Relationship Management (PRM)

Care Delivery & Telehealth

Above: Overview of the Virtual Healthcare Ecosystem — Credit: TripleTree

Insurance Disruptors

By now you are well versed in the world of French healthcare. In France, Alan is a leader with little to no competition nipping at its heels (for the time being). Two examples, from across the pond (in the US), are the closest analogs I can find: Oscar and Clover Health. Founded in 2012 and 2014, respectively, both companies are now publicly traded and working to provide solutions for private insurance and public health programs in the US. Without getting into the nitty gritty of American health policy, I think it's worthwhile to review what these organizations were (and were not) able to accomplish with all of the resources at their disposal.

🇺🇸 Oscar: Their initial product relied heavily on a functioning Affordable Care Act (Obamacare). Later they expanded into offering Medicare Plans and Oscar for Business (in which they chose to partner with Cigna, a major insurance provider). This last component is a common trend I've seen in the US, where new insurance providers aggregate/re-bundle legacy insurance products instead of creating their own. For tech, this feels like a natural first step: make something more efficient through a clean, simple user interface. If anything, it's an indicator of the inherent challenges to disrupting health insurance; something Alan managed to do in France but will likely find difficult abroad.

🇺🇸 Clover Health: Their focus is exclusively on access to Medicare. For non-US readers, Medicare is the public insurance option for the elderly. In that way, it's somewhat similar to the French system. Only imagine Alan decided to focus exclusively on the population above 65 years old. On top of that, Clover is only available in 7 states. Perhaps this speaks more to the sheer size of the country (and state-specific regulatory hurdles in the US), but it certainly demonstrates that copy/pasting the approach in France likely won't be feasible elsewhere.

Digital Front Door & Patient Relationship Management (PRM)

🇫🇷 Doctolib: Perhaps known as the OG of French health-tech, Doctolib started as a humble scheduling tool. In short, they digitized the process of booking doctor appointments. As network effects took hold (more docs & more patients on the service), they added features, like the ability to pay through the app. They pushed into telemedicine by enabling virtual appointments (a feature that unsurprisingly skyrocketed during the pandemic to 100K appointments per day, up from 1K/day prior to the health crisis 🤯 ). This is a playbook that Alan may want to follow. From a technical standpoint, they have the capabilities (+ existing data sources: doctors, patient data, mapping etc.) but unclear if they have the bandwidth. Maybe an opportunity for a partnership?

🇺🇸 PatientPop: These guys are like the CRM for doctors. Their focus is primarily on "business development" which feels like a weird term to use when speaking about your primary care physician. But ultimately, they are a business, so things like web presence, patient reviews, marketing campaigns, scheduling and task automation are important. I don't see this falling within Alan's wheelhouse, but worth reviewing to understand the various angles health tech companies are going after.

Care Delivery & Telehealth

🇺🇸 Hims/Hers: In the 2010's, there was a wave of healthcare companies disguised as tech companies disguised as consumer brands. Hims/Hers was one of them. The California-based upstart began by prescribing pharmaceutical products that were stigmatized or uncomfortable to discuss in person (balding, erectile dysfunction, acne, birth control) and made it simple and discreet. I still remember their ads plastered around the Subway in New York. Never had erectile dysfunction been so sexy! This seems like a logical (yet ambitious) next step for Alan; in fact, they must have caught JCSW's eye because he's written about the company on his Substack. Despite the logic, it's still an incredibly challenging product to get right. It requires creativity, intention, and trust. All qualities Alan has, but applying it to a completely different vertical will be tough.

🇬🇧 Babylon Health: If Alan is the little marmot 🦦 , Babylon Health is the 500 pound gorilla 🦍 . Babylon considers itself a digital-first, value based care provider that combines their AI-powered platform with virtual clinical operations. In short, they want to be the doctor's office of the future. They are based in the UK but already have operations globally. The proprietary AI may be their strongest moat. I would imagine, with the insurance platform Alan has developed, they could cut out one side of the negotiations (insurers) and build a direct to consumer telehealth tool within the existing interface. Once again, it comes down to time, resources and ability.

In short, it's impossible to cover the entire healthcare market in this piece. Hopefully the examples above rounded out your understanding of the various business models at play. Alan shows clear promise for expansion in these areas, but many smart, ambitious people are working on similar problems.

Above: Alan's global, multi-vertical ambition (and competition)

Fin

Our generation is willing to order (and pay for) virtually everything via their mobile phones:

Food

Car Rides

Furniture

Weed (I just got back from California -- they’re selling it like candy 🍭)

But for some reason, there is still so much friction when it comes to “ordering” healthcare. Now, in some cases, it’s due to the fact that you are either uninsured or under-insured (I’m looking at you America). But even with full coverage, I know plenty of people (myself included) who would much rather avoid scheduling a doctor’s appointment than deal with the implications of that single visit: scheduling, taking time off work, going to the visit in-person, filing the paperwork, getting a prescription. Besides, it’s probably nothing… just my hypochondria acting up again...

Healthcare has a long way to go in order to achieve “digital parity” with other consumer experiences. It’s one of the most critical industries in the world with the NPS (net promoter score) of a Taco Bell off the side of the interstate.

Alan solves one piece of this puzzle to date: mitigating the headache of insurance claims by bringing your insurance history to your mobile phone. Eventually, I imagine they will stake claim across the value chain. Though I’m no expert in health-tech, I do have a proprietary data-set (let’s call it a data point). As I move from employed to self-employed, I know where I’ll be signing up for health insurance 😉

🙌🏼 You made it! What next?

I'll be sending out a newsletter just like this one, every week on Tuesday. If it's up your alley, subscribe using the button below. Know someone who would love it? Share it! All of my social channels are linked below as well.

The all-in-one magic link 🔮 ➡️ Click Here

🐦 Twitter: @StartupROI & @RoiStartup 🧐 choose wisely

📸 Instagram: @startuproi

👔 LinkedIn: Startup ROI

🎁 Feedback is a gift — 📩 bonjour@startup-roi.com